TRUMP SAYS: HUNTER MAKES FORTUNE FROM SHADY DEALS!

BIDEN FAMILY STINKS TO HIGH HEAVENS OF CORRUPTION!

DON'T GET LEFT OUT: HUNTER MUST BE STOPPED!

This report was originally published by Adam Taggart at PeakProsperity

The Origins Of The Retirement Plan

Back during the Revolutionary War, the Continental Congress promised a monthly lifetime income to soldiers who fought and survived the conflict. This guaranteed income stream, called a “pension”, was again offered to soldiers in the Civil War and every American war since.

Since then, similar pension promises funded from public coffers expanded to cover retirees from other branches of government. States and cities followed suit — extending pensions to all sorts of municipal workers ranging from policemen to politicians, teachers to trash collectors.

A pension is what’s referred to as a defined benefit plan. The payout promised a worker upon retirement is guaranteed up front according to a formula, typically dependent on salary size and years of employment.

Understandably, workers appreciated the security and dependability offered by pensions. So, as a means to attract skilled talent, the private sector started offering them, too.

The first corporate pension was offered by the American Express Company in 1875. By the 1960s, half of all employees in the private sector were covered by a pension plan.

Off-loading Of Retirement Risk By Corporations

Once pensions had become commonplace, they were much less effective as an incentive to lure top talent. They started to feel like burdensome cost centers to companies.

As America’s corporations grew and their veteran employees started hitting retirement age, the amount of funding required to meet current and future pension funding obligations became huge. And it kept growing. Remember, the Baby Boomer generation, the largest ever by far in US history, was just entering the workforce by the 1960s.

Companies were eager to get this expanding liability off of their backs. And the more poorly-capitalized firms started defaulting on their pensions, stiffing those who had loyally worked for them.

So, it’s little surprise that the 1970s and ’80s saw the introduction of personal retirement savings plans. The Individual Retirement Arrangement (IRA) was formed by the Employee Retirement Income Security Act (ERISA) in 1974. And the first 401k plan was created in 1980.

These savings vehicles are defined contribution plans. The future payout of the plan is variable (i.e., unknown today), and will be largely a function of how much of their income the worker directs into the fund over their career, as well as the market return on the fund’s investments.

Touted as a revolutionary improvement for the worker, these plans promised to give the individual power over his/her own financial destiny. No longer would it be dictated by their employer.

Your company doesn’t offer a pension? No worries: open an IRA and create your own personal pension fund.

Afraid your employer might mismanage your pension fund? A 401k removes that risk. You decide how your retirement money is invested.

Want to retire sooner? Just increase the percent of your annual income contributions.

All this sounded pretty good to workers. But it sounded GREAT to their employers.

Why? Because it transferred the burden of retirement funding away from the company and onto its employees. It allowed for the removal of a massive and fast-growing liability off of the corporate balance sheet, and materially improved the outlook for future earnings and cash flow.

As you would expect given this, corporate America moved swiftly over the next several decades to cap pension participation and transition to defined contribution plans.

The table below shows how vigorously pensions (green) have disappeared since the introduction of IRAs and 401ks (red):

(Source)

So, to recap: 40 years ago, a grand experiment was embarked upon. One that promised US workers: Using these new defined contribution vehicles, you’ll be better off when you reach retirement age.

Which raises a simple but very important question: How have things worked out?

The Ugly Aftermath

America The Broke

Well, things haven’t worked out too well.

Three decades later, what we’re realizing is that this shift from dedicated-contribution pension plans to voluntary private savings was a grand experiment with no assurances. Corporations definitely benefited, as they could redeploy capital to expansion or bottom line profits. But employees? The data certainly seems to show that the experiment did not take human nature into account enough – specifically, the fact that just because people have the option to save money for later use doesn’t mean that they actually will.

First off, not every American worker (by far) is offered a 401k or similar retirement plan through work. But of those that are, 21% choose not to participate (source).

As a result, 1 in 4 of those aged 45-64 and 22% of those 65+ have $0 in retirement savings (source). Forty-nine percent of American adults of all ages aren’t saving anything for retirement.

In 2016, the Economic Policy Institute published an excellent chartbook titled The State Of American Retirement (for those inclined to review the full set of charts on their website, it’s well worth the time). The EPI’s main conclusion from their analysis is that the switchover of the US workforce from defined-benefit pension plans to self-directed retirement savings vehicles (e..g, 401Ks and IRAs) has resulted in a sizeable drop in retirement preparedness. Retirement wealth has not grown fast enough to keep pace with our aging population.

The stats illustrated by the EPI’s charts are frightening on a mean, or average, level. For instance, for all workers 32-61, the average amount saved for retirement is less than $100,000. That’s not much to live on in the last decades of your twilight years. And that average savings is actually lower than it was back in 2007, showing that households have still yet to fully recover the wealth lost during the Great Recession.

But mean numbers are skewed by the outliers. In this case, the multi-$million households are bringing up the average pretty dramatically, making things look better than they really are. It’s when we look at the median figures that things get truly scary:

Nearly half of families have no retirement account savings at all. That makes median (50th percentile) values low for all age groups, ranging from $480 for families in their mid-30s to $17,000 for families approaching retirement in 2013. For most age groups, median account balances in 2013 were less than half their pre-recession peak and lower than at the start of the new millennium. (Source)

The 50th percentile household aged 56-61 has only $17,000 to retire on. That’s dangerously close to the Federal poverty level income for a family of two for just a single year.

Most planners advise saving enough before retirement to maintain annual living expenses at about 70-80% of what they were during one’s income-earning years. Medicare out-of-pocket costs alone are expected to be between $240,000 and $430,000 over retirement for a 65-year-old couple retiring today.

The gap between retirement savings and living costs in one’s later years is pretty staggering:

As for Medicare, the out-of-pocket costs could easily soar over retirement. The Wall Street Journal reports that the current estimate of Medicare’s unfunded liability now tops $42 Trillion. Such a mind-boggling gap makes it highly likely that current retirees will not receive all of the entitlements they are being promised.

And the denial being shown by baby boomers entering retirement is frightening. Many simply plan to work longer before retiring, with a growing percentage saying they plan to work “forever”.

But the data shows that declining health gives older Americans no choice but to leave the work force eventually, whether they want to or not. Years of surveys by the Employment Benefit Research Institute show that fully half of current retirees had to leave the work force sooner than desired due to health problems, disability, or layoffs.

Add to this the nefarious impact of the Federal Reserve’s prolonged 0% interest rate policy, which has made it extremely hard for retirees with fixed-income investments to generate a meaningful income from them.

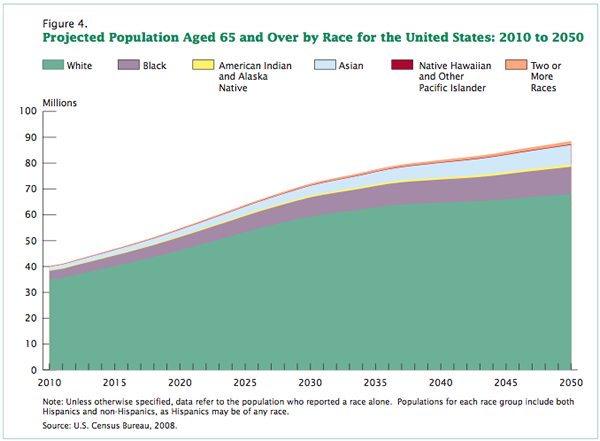

The number of Americans aged 65 years and older is projected to more than double in the next 40 years:

Will the remaining body of active workers be able to support this tsunami of underfunded seniors? Don’t bet on it.

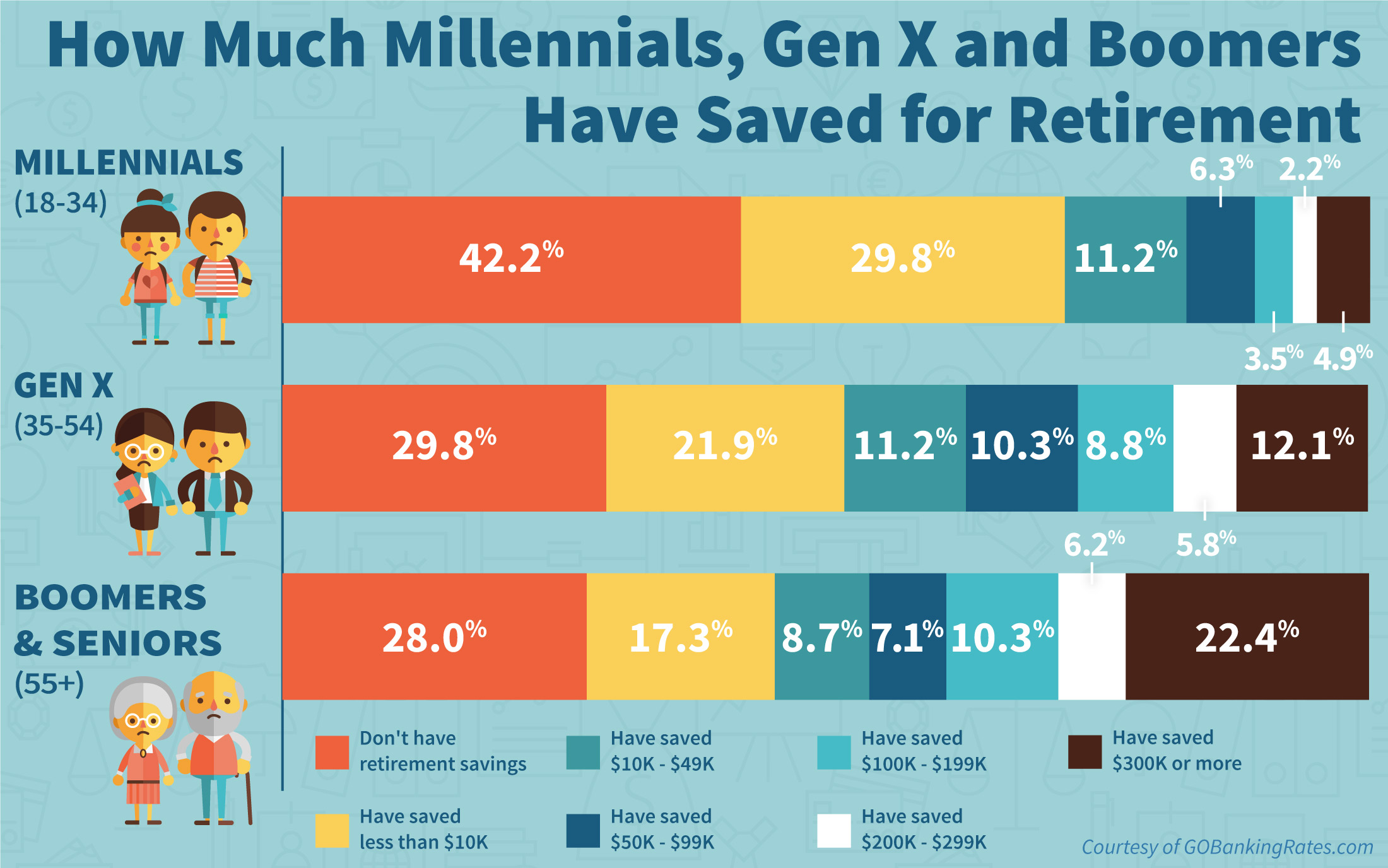

Especially since their retirement savings prospects are even more dim. With long-stagnant real wages and punishing price inflation in the cost of living, Generation X and Millennials are hard-pressed to put money away for their twilight years:

Public Pensions: Broken Promises

And for those “lucky” folks expecting to enjoy a public pension, there’s a lot of uncertainty as to whether they’re going to receive all they’ve been promised.

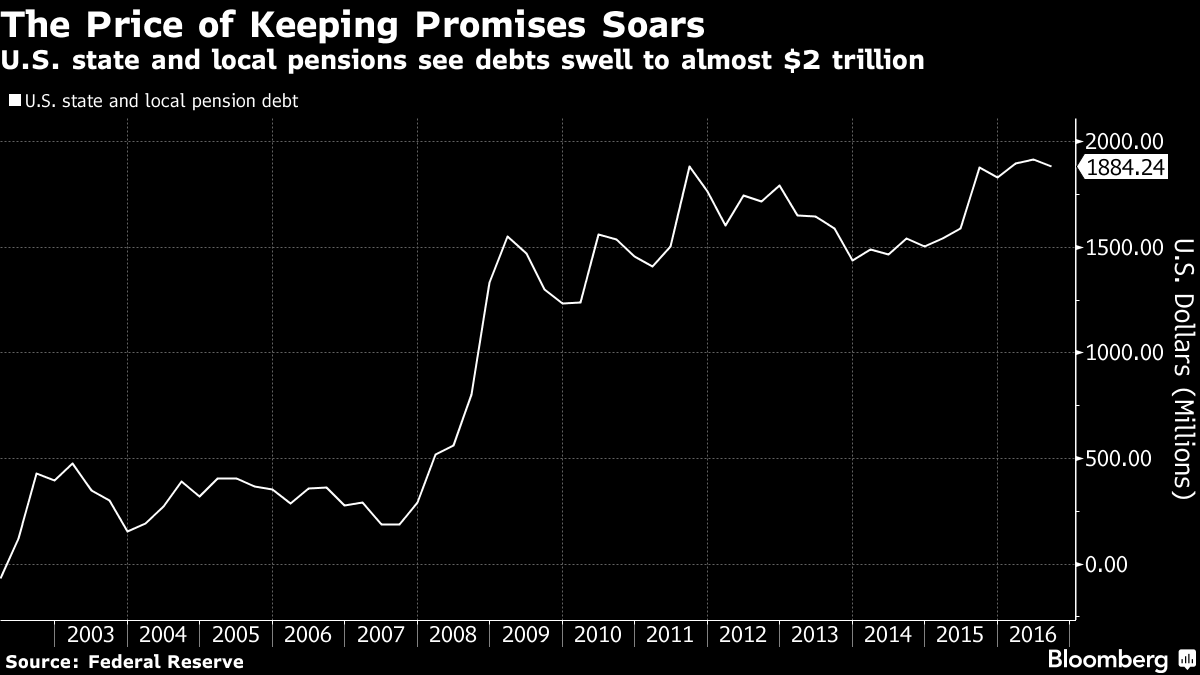

Due to underfunded contributions, years of portfolio under-performance due to the Federal Reserve’s 0% interest rate policy, poor fund management, and other reasons, many of the federal and state pensions are woefully under-captialized. The below chart from former Dallas Fed advisor Danielle DiMartino-Booth shows how the total sum of unfunded public pension obligations exploded from $292 billion in 2007 to $1.9 trillion by the end of 2016:

(Source)

And the daily headlines of failing state and local pension funds (Illinois, Kentucky, New Jersey, Dallas, Providence — to name but a few) show that the problem is metastasizing across the nation at an accelerating rate.

Affording Your Future

The bottom line when it comes to retirement is that you’re on your own. The vehicles and the promises you’ve been given are proving woefully insufficient to fund the “retirement” dream you’ve been sold your whole life.

That’s the bad news.

But the good news is that the dream is still attainable. There are strategies and behaviors that, if adopted now, will make it much more likely for you to be able to afford to retire — and in a way you can enjoy.

In Part 2: Success Strategies For Retirement, we detail out these best practices for a solvent retirement, including providing 14 specific action steps you can start taking right now in your life that will materially improve your odds of enjoying your later years with grace.

For far too many Americans, “retirement” will remain a perpetual myth. Don’t let that happen to you.

Click here to read Part 2 of this report (free executive summary, enrollment required for full access)

It Took 22 Years to Get to This Point

Is it finally "transmitting" between humans? A second person in Missouri has been confirmed as...

This article was originally published by Connor O'Keeffe at The Mises Institute. Last week, the...

Twenty-four-hour diner and breakfast restaurant Denny's recently announced the closure of 150...

Commenting Policy:

Some comments on this web site are automatically moderated through our Spam protection systems. Please be patient if your comment isn’t immediately available. We’re not trying to censor you, the system just wants to make sure you’re not a robot posting random spam.

This website thrives because of its community. While we support lively debates and understand that people get excited, frustrated or angry at times, we ask that the conversation remain civil. Racism, to include any religious affiliation, will not be tolerated on this site, including the disparagement of people in the comments section.

The new crisis? Homeless seniors. By the millions. Your retirement money went to the immigrants. Act accordingly.

Totally true: if people knew how much is being spent on immigrants and refugees, and where that money is coming from, they would puke.

Hey, at least Bill Clinton gets laid tons and the poon couldn’t get finer!

i don’t know….i would rather wake up in a sleepin’ bag with barney fwank than THAT B**** he “lives with”.

BCD, I’m pretty sure that even Hillary gets more pussy than Bill gets.

Oh Snap!

The whole thing is bogus; when, ever, does an 18 year old have anything saved for retirement? When I was 18 I had $2500 saved up from summer jobs and spent all of it and more going to school. Finally got a job when I was out at 21 plus had to borrow money to buy a car. So at 22 I had less than nothing. Retired now with close to $3,000,000. (Counting cash flow values) I saved over half of my after tax earnings You cannot spend it and have it. How many billions of $3 a cup coffee does Starbucks sell? I don’t know never bought one. Let them eat cake.

All those that absolutely must have the newest iPhone, daily lattes, facials, tatoos, noserings, body piercings, cigarettes, etc, then complain about living paycheck to paycheck with no savings can all go fuck themselves.

There’s nothing I hate more than my patients showing me an image of their medicaid card on the latest Iphone.

2 thumbs up!

I don;t know how half those people can get a job. Face tattoos, nose rings. Half dollars in the ears. Gross!

What a bunch of crap. Are you saying the system works or does not? Because I can’t tell. You have to be some kind of pathetic government troll by the obtuse way you write.

My vote is that the system is broken. Retirement and pensions were purged when manufacturing left the U.S. starting in the mid-70s.

I saved for a car. Once I spent that money on a car then I had to make more money to support the car, and then more money to replace the car.

I saved but lost it all paying 80-percent for my college education. Graduated broke into several meaningless jobs. The promised real jobs in high tech and top-one-hundred companies were out-sourced, so after a few years of full employment, I was unemployed again using savings to find another job.

I put 20-percent of my gross income into a 401K only to see 40 to 50-percent just disappear in the Crash of ’08 – ’09 mainly because my old-age-nest-egg was exposed to risk by these banksters. What was left of my 401K was taxed 34-percent.

In the U.S. the mandatory belief system said that a man has two choices — work or prison. Now try that again but in a country that has no jobs.

“Are there no prisons? Are there no work houses?”

My great grandparents and my grandparents got the raw deal. The rich elites, the MSM, and the professional politicians are about to pull that crap again on a population that still remembers. Do they want to go back to the thrilling days of yester-year?

The problem is simple: trust. In order to commit to saving some portion of your income with a fund, you have to trust that it will be there in 40 years time. But, as people have learned from hard experience, the chances of that happening have reached nearly zero. The saving and investment system is broken. Trust is evaporated. The last surviving redoubt in the system is lifelong government employees, who have the only platinum pension schemes left.

As somebody discovered when they researched how the economy really works, they found the government (and civil servants) and the stock market are now like two criminals handcuffed together. They have to do everything together. That means government must do whatever it can to juice the stock market and bail out banks and financials when they screw up. If they do not, then their pension plans get smoked. This means government does not longer care about the public good but instead is focused on the markets. In this arrangement, everyone else can go to hell.

The biggest problem lately is that the rate of inflation is surpassing the earnings of the retirement funds.

Since 1913, and the creation of the FED, the value of the dollar has fallen between 93 to 98-percent. Unfortunately, we happen to be living in that time when the value of the dollar falls to zero.

The bad habits that caused the Crash of ’08-’09 are still in play. Nothing has changed, except that the banksters have doubled down on screwing the American people.

Now add Zero Interest Policy (ZIRP) on top of this and the long national nightmare starts to get really interesting.

Good comment. Spot on.

Charlie Rose canned for sexual harassment. Those that claim publicly that they and their ideology have the moral high ground, are usually the biggest pervs.

I’m thinking there is a coup in the radical left. The old guard is being flushed. The sexual thing is interesting, but it’s just a tool. It’s mainly a bunch of old guys being targeted. Charlie Rose had a lot of power, he’s also 75 years old.

The left has been getting their collective butts kicked. Expect them to discard the old guard and reorganize. It’d be nice if the left got violent and they also take out some in friendly fire. Beware of who takes power behind the scenes.

Agreed, the radical left is kicking the moderate left to the curb. Revolution is in order.

Charlie Rose (the great saint that he is) really tried to stick it to Steve Bannon during their 60 Minutes interview:

http://www.youtube.com/watch?v=Hz9FqepcRUM

a great site for news on pension shortfalls.

pensiontsunami.com

🙂 another add to my reading list

thanks grammy…subscribe and get stories sent every week or so….it’s a great resource for failed pensions.

We are a nation in decline. And sadly the Make America Great Again slogan will not happen. Most pensioners where government employees & parasite takers any how. I could care less if they don’t get any pension.

I agree Old Guy. I am a self-employed man. Been so most of my working life. A life I actually hope is the one I live until I die in the traces. There’s a sign painted on the side of a fish-house near me that reads, “Work – the activity that gives meaning to a man’s life”. And it does. I despise men and women who say they hate to work. I get enjoyment, satisfaction, pride and a sense of reason for living out of what I do. It is like the kids growing up and in school worrying about grades. It is not the grade that counts. It is what you retain, have really learned and can apply that is the important thing. Once, a teacher of mine, she told me at the end of the year that if I passed her class she expected me to be able to turn out around as soon as I passed out the door and be able to walk to the front of the classroom and teach the course. For that is what education is supposed to be. A passing on of knowledge. Just as work is supposed to be for improvement of whatever problem or the solution to whatever task you’ve been set. The paycheck is secondary. It will come and go. But the effort, the skill, the quality will be something that hopefully will live on. So? Screw pensions and retirement. Not for me. I don’t want to quit.

My retirement was earned. I contributed 7% of my paycheck pre tax for 20 years. So why are pension funds running out when you only get paid for what you put in, nothing more.

People think that pensions are this magical gift that keeps on giving with no contributions.

This ENTIRE country is a huge, massive cluster unless you are one of the 1%, hell you have no worries under the sun. For the rest of us average suckers, just surviving and making ends meet is beyond a damn challenge. Most people literally have $0 to put towards retirement. What in the world is going to happen to the MILLIONS that are going to be not only broke, hungry but also with NO roof over their heads? What then? Maybe put out those that are no even god damned citizens and claim what they have stolen from us who actually have to foot the fleecing bill year after year. It is just disgusting.

The disability pension for VA is $1,075 a month for veterans judged unable to work. This has not been raised outside Social Security COLAs since 1978. Meanwhile the dollar purchasing power ekes away steadily.

70-100% service connected disabled single vet is $1338 – $2915 per month for 2017. In my CBOC I’ve only seen one guy that might fit the 100% disabled. We don’t have a VA medical hospital here so I don’t see the bad cases. Most of us at the CBOC are service connected disabled of varying percentages, but can and do work. I saw an entry for payment of $133 for 10% disabled, I have to look into that, I thought you have to be at least 30% to get money.

ht tps://www.benefits.va.gov/COMPENSATION/resources_comp01.asp#BM03

All things considered it is really not that much money, for what it cost the soldier.

Yes 10% ers get 133 as of the last COLA, but they still take it out of my retirement and send it back as tax free, those 50% or better don’t have anything taken out, just get an added payment.

I retired in 91 with over 27 yrs, ended up with some final Dr that had just had a stroke and was giving me my final evaluation, well that worked out well. So since 91 all I’ve gotten is 10% disability. But I don’t complain, and don’t feel like kissing any ass, they had my records.

And yeah I’m a VN vet btw,have fought facial, back and chest rash’s since I came back, for 30 years they couldn’t figure out what was causing them, one Dr called it “old man’s decease”, lol, smirk, I said OK so 23 is considered old?

They gave me 2 hearing aids, said that was my compensation for the hearing loss, which have been lost long ago anyway. The other odds and ends were just ignored.

All I bother going to the VA for now is eye exams every 18mo to 2 years for the glasses, screw the rest of it.

My buddies keep telling me to go nuts and claim PDSD, that it was the quickest way to go 100%, I said Fuck em…….

anyone probably under 65 is screwed.

even those that have savings are screwed.

do you think those that did nothing won’t vote to take yours for themselves ? if so, you haven’t been paying attention to medicare, obamacare and welfare. every one of them has increased while the number of people paying taxes has decreased.

we’re at the pinnacle of lifestyle for western civilization, the decline is going to be quick and brutal.

So, what country would you recommend Americans migrate to for better future living conditions?

Im one with no retirment at all, pulled it all out. Glad i could help that statistic. I have a tiny savings also that fits in with the data. Course theres always that chance a few of these people are going debt free and are saving in untraceable assets. If you have anything that can be counted as a statistic, then it can also be taken.

Thank heaven i have no credit card debt, how many of these guys are making 5% on retirment and paying 20% on credit card. Shoot my last statment from my retirment fund was a measly 1.2%. I like dave ramsey’s method of saving money, except for his unicorn 10% return for life crap on mutual funds.

I pray everone makes it through the next round of turmoil because money is not going far, it seems everyone is being stretched thin. Cutting down to just bare necessities will just keep you afloat these days.

Might as well have holes in your pockets. Spread the poor.

Due to health problems I retired at age 55. I started working at age 8(self employed) and paying into SS starting at age 16. I do not collect any government money( although I’m now able to collect Social security if I choose). I survive on private pensions. I typically save 10% of my pension income.

I did this by judicious selection of employers( my skills and education are highly sought after), I only bought used cars, my homes were VERY humble, where possible I fix or build everything myself, I save money, and I’ve been debt free since 1992.

My advice – learn a trade or two, or more, spend some time in the military, and get a STEM degree(get the military or employer to pay for it). Never buy a new car, house, or boat, always buy used. Pay off your debt and save/invest all the money you would have spent on servicing debt. Get used to living on 75% of your net income at as early an age as possible and prepare for SHTF events. You will easily be able to retire barring “Black Swan” events eg. divorce, catastrophic illness, un-insured disasters, et al.

It is not as easy as I make it sound and it requires a bit of luck,

but it is better than eating cat food when you are old because you drove the fanciest cars and had the nicest home in the best neighborhoods when you were young.

“Afraid your employer might mismanage your pension fund? A 401k removes that risk. You decide how your retirement money is invested.” And don’t worry, they’ll steal that too… thru ZIRP, high taxes, bail ins, etc.

“Want to retire sooner? Just increase the percent of your annual income contributions.” Yep. And they’ll steal THAT, too.

But don’t worry about pensions! In IL. the Supreme Court ruled those MUST be paid – even tho there is no money. This includes folks like a family member I know, a regular teacher in elementary school, who retired making $110k/yr – complete with a zillion sick days (I get ZERO in my job), two weeks at Christmas, 3 months in the summer, etc.(I have no paid vacation, no sick days… gotta pay for these lazy slobs) She retired early at 56, and makes $7k/month sitting on her brobdignagian derriere doing NOTHING – possibly for up to half a century. I get to pay MASSIVE property taxes to support this stuff. How nice. Here’s the pension database for IL. Read it and vomit: https://www.bettergov.org/pension-database

But here’s the kicker. I have to remain in the Socialist Workers’ Paradise of IL. to take care of a very elderly mother (the retirees are too freaking lazy to do it, of course). But once she is gone, I will be voting with my feet. All these socialists can then try to live off of each other. After all it worked SO very well in places like Detroit, didn’t it!

The second chart shows most people lost their shirt in 2007/8 the market collapsed and from the look of the chart they pulled their money out at the bottom. Their 401K accounts never recovered even though the stock market did.

I have to say, I saw it happening and got out of mutual funds and bought back in at the bottom. I did quite good. My 401K is now mostly out of stocks again with them in nose bleed territory again.

While I was Making those moves, I took the opportunity to consolidate a couple 401 K accounts from multiple employers I had, and thereby cut fees, I now have one account at a brokerage, I can manage it and buy literally any stock or fund I want. The latest stock I did buy was “Home Depot”, the day the first hurricane hit. It’s up smartly and just raised its dividend. There will likely be a year long reconstruction effort where the three hurricanes hit. There will be lots of government and insurance money spent at HD.

Is there any statistics on just private pensions as compared to the public sector pensions? How would they compare? People always talk about the public pensions which implies lumping the private ones into them are just as bad.

i would bet pensiontsunami.com would be able to answer that one.

Save like there is no other option. The government can’t and won’t bail you out like the banks and corporations. No debt and living on less will save you later.

That is my approach. Save as much as I can and keep stacking PMs.

Before any armchair heroes try to crucify me, I am saying this is only a theory or model. It is not a fixed law of nature, per se. Or, it is not the way of the world, as we know it —

https://en.wikipedia.org/wiki/Social_contract

The (unwritten, imaginary) social contract has two sides, in which the labor and the establishment are obliged, equally.

You’re putting the onus on so many untermenschen, telling us how irresponsible they were, even though unhindered cooperation, to the utmost, was no guarantee of success.

A slave (one who is called that, plainly), a beast of burden, or inanimate tool, are all entitled to shelter, maintenance, repairs, transportation to the work site…

Benign neglect would be considered a failure of the social contract, assuming that totalitarianism is supposed to come with benefits.

Not providing for your biological function — even if you were just dumb brutes, and nothing more — is no morally different than asking you to work without air or in hot lava or in a stampede of buffalo, piranha tank…

They’re telling passive, moral agents that everything is your fault, when a dictatorship is responsible to remove the element of risk from the system.

Benjamin Franklin once said: “Those who would give up essential Liberty, to purchase a little temporary Safety, deserve neither Liberty nor Safety.”

You didn’t expect the freedom OR the safety, when one is generally traded for the other.

I have resigned myself that I will work until I die. Very simple. I do not believe Social Security will be there when I retire at 67. Nor do I beleive an IRA will be there. I do beleive the government will take that once SS goes bankrupt and enough people riot in the streets for “their” money.I have a neighbor on disability who refers to her government check as “my payday”. I think I’ve said enough.

I already decided on how I will do retirement: I will go to somewhere in Asia that is cheap, beautiful and has lots of young women. I will build a simple home with some spare rooms where some of these young women can live – for a fee. I will require daily massages and sex and that’s it. I have calculated I can do this for much less than living in the US. I can afford private healthcare for when I need it and will visit Switzerland every year for a check-up.

Why in hell would I rot in the US, be abused by beastly black nurses, eat garbage food, and be poisoned by the toxic drugs they peddle to the old?

Better to live somewhere where they respect the old and do not look down on a horny old man who likes his comforts.

Frank,

If my wife of 40 years were to die on me, I would consider, following your lead!

Have a friend who is now retired from a good job. This guy worked hard all his career and successfully raised children. He is a world expert in his field. But his reward for all of that is to be shackled to a cranky wife who I see bicker and henpeck him all the time. I can tell they no longer have sex. He keeps fit and is a good looking guy. I know he likes the Asian women and have tried to nudge him to take a trip there and have some fun. It would so help relieve the tension in his life and he deserves the pleasure after being a hard-working guy for all those decades.

Watch out. Those little yellow ladies may scam you.

http://www.youtube.com/watch?v=QuILfAZ3jWQ

Southside,

You must be young. SS will never go “broke”, but everyone will get a reduction in payments around 2032 or so, if we can’t fix our Democrat problem. The fact that Democrats exist is the problem.

I’ve had a 401K, 403b, and an IRA. These all are pretty safe ways to save for retirement, if you keep an eye on them, and the government. Keep a plan to convert those investment vehicles to something the government won’t mess with, assuming we still have a government.

I can’t recommend a way to safe guard your wealth. Some like PM’s, some like physical assets( land, structures, animals, tools, and transportation ), some like cash and going “Galt”, some study and use the “system”, I favor a mix.

Good luck, I don’t thinks things are as dark as is it seems,

as long as you prepare and assume the worst from our government.

Rellic,such a compliment! I’m 57 years young,fit,and good health. Praise God.

Oh it will be there. Will what you get be worth anything? Probably not. You will get peanuts and be told to be happy.

Inflation is the cruelest tax of all.

Gold is the great inflation fighter.

Can someone advise please me? Im 32 and work for a manufacturing company that has a 401k that will match 50% up to 8% on earnings. I always contemplate starting one or not.

I see my coworkers and friends have 100,000 already in their 401k after 10 or less years. I just dont know if i should start one or not. I for one believe that by the time i retire, there will be 0 dollars for anyone who has any retirment plan. But then the other side of me knows that i should prepare for retirement in some way, and only contribute what i could theoretically “afford” to lose, should SHTF. I feel left out because i dont have 100,000 saved up like my friends do. But will all of that money be there in 30 years? Just some of it? I do believe in investing in other things as well…..but nothing is guaranteed.

What should i do?

What should i do?

Contribute at least as much as you can to receive your employer’s match (that is free money). In 2018, you can contribute up to $18,500 (if married) pre-tax to your 401(k) account. Doing this will lower your taxable income, and may put you in a lower federal income tax bracket.

There are gold-related funds, such as TGLDX, that may be available in your 401(k) suite of investment options. The other thing to consider is that you can roll over your 401(k) to an IRA if you should leave that employer. When you do that, you greatly increase the investment options available (since you will no longer be limited to just those investments in your employer’s plan).

Bloomburg just published an article that talks about people who lost mobile homes in the hurricane. Apparently few can afford to replace them because mobile home prices have inflated at close to 10% a year for the last five years. Expect to pay $140,000 to remove the old double wide and replace it with a new one. Most of these people are on fixed incomes, and insurance is leaving them short.

If you think black lives have no value in our society, you should try old, poor, and in bad health.